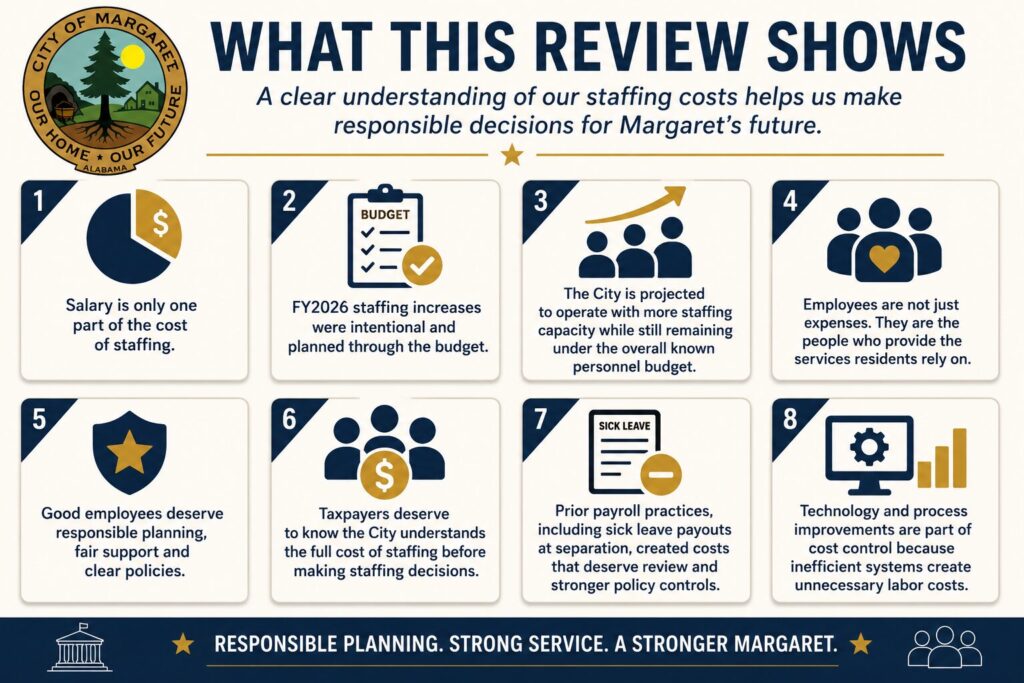

Understanding the True Cost of Municipal Government

One of the questions I was asked recently was:

“How much do City employees cost?”

That is a fair question, but it is also one that has to be answered carefully.

City employees are not just numbers in a budget. They are the people who answer calls, respond to emergencies, maintain roads and utilities, process permits, handle court records, inspect construction, manage finances, keep parks and public spaces usable, and help residents solve problems every day.

I am thankful for the employees who serve the City of Margaret. Many of them work in difficult conditions, respond after hours, deal with problems most residents never see, and carry responsibilities that are easy to overlook until something goes wrong.

At the same time, because employee costs are one of the largest parts of municipal government, taxpayers deserve to understand what those costs include and how the City plans for them.

At first glance, most people assume the answer is payroll.

If an employee earns $20 per hour, it is easy to assume the City’s cost is simply $20 for every hour worked.

The reality is far more complex.

For every employee, the City also pays Social Security and Medicare taxes, retirement contributions, health insurance, workers’ compensation insurance, unemployment costs, training expenses, uniforms, equipment, software licensing, vehicles, fuel, office space and other support costs. The hourly wage is only one part of the total cost required to provide municipal services.

Employees are an investment, and that investment must be planned, budgeted and managed responsibly.

The FY2026 budget was built with that understanding.

The goal was not simply to approve payroll. The goal was to understand the full cost of staffing, plan for it, budget for it and use those resources to improve services for the people of Margaret.

A Different Approach to Budgeting

FY2025 did not provide a strong model for long-term staffing or operational planning.

The City was operating, but the budget did not clearly show the full cost of building the departments we actually needed.

FY2026 was different.

The staffing increase was intentional. The budget reflected that intention. The goal was to build capacity in public safety, public works, administration, inspections and court operations while understanding the cost that comes with it.

That matters because a city cannot responsibly expand services if it does not understand what those services actually cost.

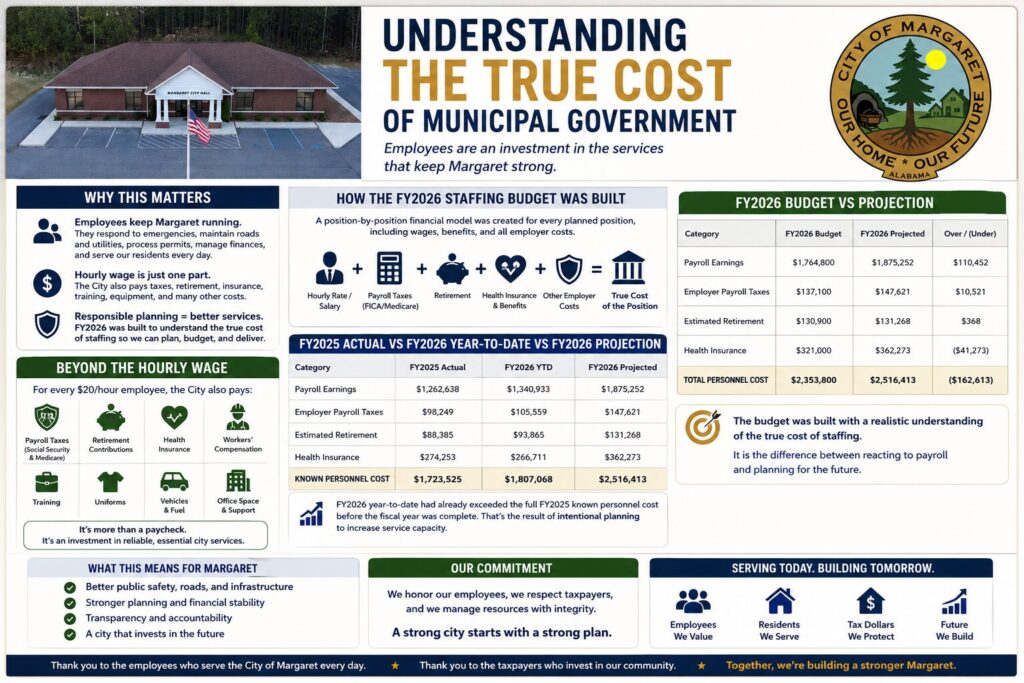

How the FY2026 Staffing Budget Was Built

The FY2026 staffing budget was not built by simply increasing last year’s payroll number.

It was built position by position.

For each planned position, the City reviewed the expected employment status, scheduled hours, hourly rate or salary, monthly wage cost, employer payroll taxes, retirement, insurance, unemployment and other benefit-related costs.

That matters because a staffing plan is not just a list of names or hourly wages. It is a financial model showing what it actually costs to operate each department.

The staffing model included as much of the employee cost categories that could be identified. Many take time to determine such as vehicle cost per position, fuel, etc.

This is the difference between reacting to payroll and planning for staffing.

A $20-per-hour employee does not cost the City only $20 per hour. Once payroll taxes, retirement, insurance and other employer costs are included, the true annual cost can be significantly higher.

That is why the FY2026 budget was built around the full cost of staffing, not just wages.

These calculations are not meant to reduce employees to numbers. They are meant to make sure the City is budgeting responsibly for the people who provide services.

Good employees deserve more than improvised budgeting. They deserve a plan that accounts for their wages, benefits, training, equipment, tools and support systems.

Taxpayers also deserve to know that when the City adds staffing, it understands the full cost of that decision before making it.

That is what this budget process was designed to do.

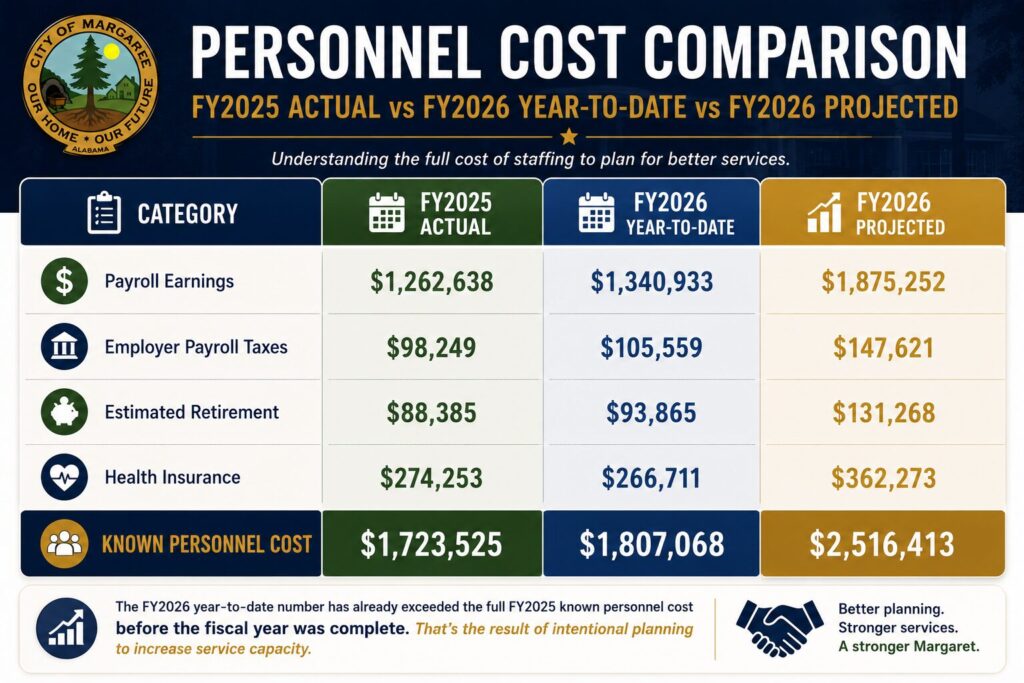

FY2025 Actual vs FY2026 Year-to-Date vs FY2026 Projection

The table below shows the measurable personnel cost comparison between FY2025 actual results, FY2026 year-to-date activity and the current FY2026 projection through September 30.

The FY2026 year-to-date number had already exceeded the full FY2025 known personnel cost before the fiscal year was complete.

That was not accidental.

FY2026 was budgeted with the knowledge that staffing costs would increase because the City had a plan to increase service capacity.

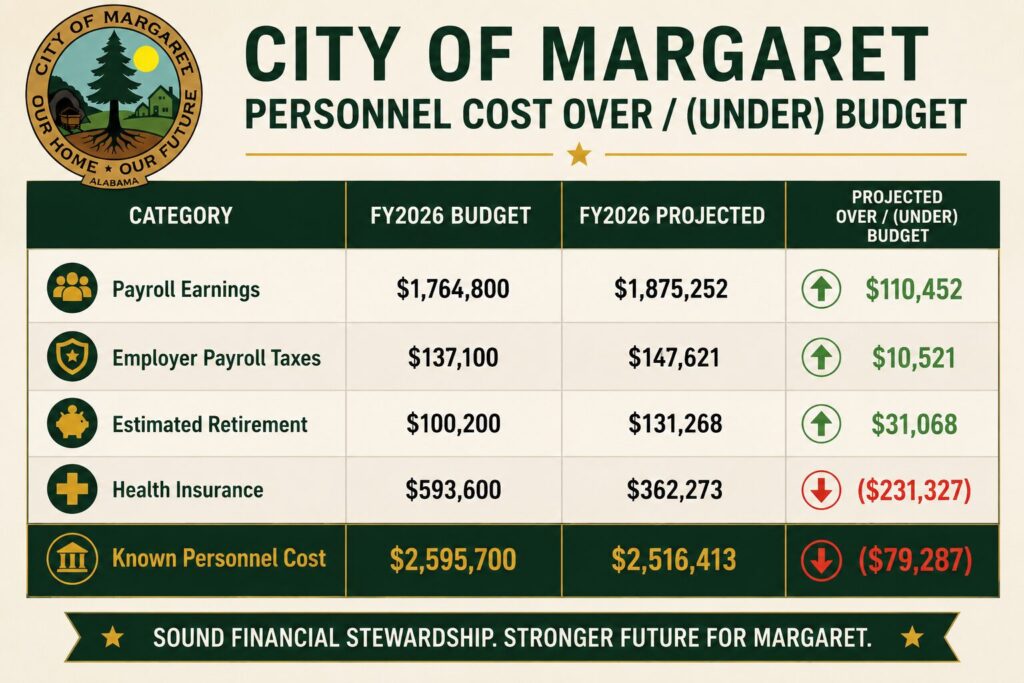

FY2026 Budget vs FY2026 Projection

The budget is where the planning becomes clear.

The City budgeted for increased staffing and the supporting costs that come with it.

The projection shows that payroll, payroll taxes and retirement are trending above the individual budget lines, while health insurance is trending significantly under budget.

That is important.

It shows the City budgeted conservatively for the full burden of staffing, while the actual staffing mix of full-time, part-time and non-benefit positions is projected to keep total known personnel cost under the overall personnel budget.

In other words, the City did not stumble into higher staffing costs.

The City planned for increased staffing, budgeted for it and is currently projected to remain within the overall known personnel budget.

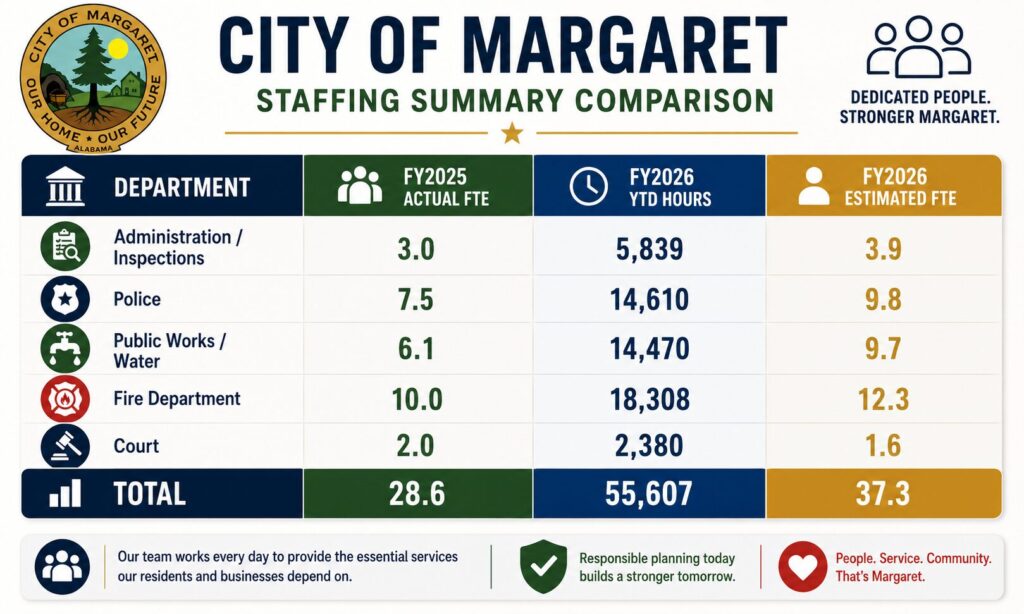

Staffing Measured by FTE

Headcount can be misleading.

If one employee leaves and another employee fills the same role, payroll may show two different people, but operationally that is one position.

That is why the better way to compare staffing is by full-time equivalent, or FTE.

For this article, one FTE equals 2,080 hours per year. This helps show how much actual staffing capacity the City had, rather than simply counting every person who appeared in payroll.

This table shows the real staffing story.

FY2025 operated at approximately 28.6 FTE across these major departments.

FY2026 is projected to operate at approximately 37.3 FTE.

That is an increase of about 8.7 FTE.

That increase was intentional.

It was part of the FY2026 budget plan.

The purpose was to give departments enough capacity to provide the level of service residents expect from a growing city.

People, Not Just Positions

It is important to say this plainly: FTE calculations are a budgeting tool, not a measure of an employee’s value.

The City uses FTE to understand staffing capacity, compare years fairly and avoid overstating personnel numbers when one person leaves and another person fills the same role.

But behind every FTE number is real work being performed by real people.

A police shift covered, a fire call answered, a road repaired, a permit processed, a water issue addressed, a court file handled, a financial report completed or a resident helped at City Hall all require people.

The purpose of this review is not to reduce employees to numbers.

The purpose is to show that if the City expects professional, reliable and responsive services, then it must also budget honestly for the people who provide those services.

What the Staffing Increase Accomplished

The staffing increase was not about growing government for the sake of growth.

It was about building departments that can function.

The Fire Department has made significant progress and now operates at a higher level of service than in previous years. The department has achieved Advanced Life Support, or ALS, capability. That means advanced emergency medical care can begin sooner and the level of service available to residents is higher.

That does not happen without people.

It requires personnel, training, certification, equipment and ongoing support.

The Police Department also required a more realistic staffing model. A police department cannot provide reliable coverage if it is constantly trying to patch shift gaps. More appropriate staffing allows the City to improve police presence, improve coverage and reduce the strain that comes from relying too heavily on the same officers to cover every need.

Public Works and Water also require practical staffing capacity. Roads, drainage, utilities, maintenance, parks, city facilities and day-to-day service requests do not maintain themselves.

Administration, inspections and court operations also require staff time. Permits, records, financial management, court processing, reporting, inspections, citizen service and compliance work are all part of running a functioning municipal government.

The point is simple.

Staffing is not just a cost.

Staffing is capacity.

The FY2026 budget was built to create more capacity.

An Important Note About Sick Leave Payouts

While reviewing payroll and personnel costs, I noticed something worth sharing with the public.

Right after my administration took office, I identified an instance where the former administration had approved sick leave being paid to an employee who was leaving employment.

That raised a concern because paying out accumulated sick leave when someone leaves employment is not normal unless it is clearly authorized by adopted policy, contract or council action.

After reviewing more records, we found additional sick leave payments made when employees separated from City employment. In FY2025 alone, payroll records show more than $22,000 paid under sick leave classifications. Some of those payments involved large blocks of accumulated sick leave, including payments of more than 100 hours at a time.

That is real money.

It is also an example of why personnel policies matter.

The issue is not whether employees deserve fair benefits. They do.

The issue is that benefits must be clearly defined, properly authorized, consistently applied and budgeted.

When benefits are not clearly managed, they can create taxpayer costs that were never properly planned.

This is one of the reasons we are reviewing personnel policies and payroll practices carefully. A city cannot manage what it does not measure, and it cannot protect taxpayers from unnecessary long-term costs if those costs are hidden inside payroll practices.

The Cost of Benefits and Future Obligations

Employee benefits are part of the true cost of staffing.

They help recruit and retain qualified employees, but they also create financial obligations that must be understood.

The lesson is simple.

Employee costs do not stop at wages.

They include taxes, retirement, insurance, leave, training, equipment, vehicles, software and long-term obligations created by policy.

Other Budget Facts That Matter

Personnel cost is the largest part of this discussion, but it is not the only cost of operating departments.

A police officer needs more than a paycheck. A firefighter needs more than a paycheck. Public Works employees need more than a paycheck. Administrative and court staff need systems, software, tools and support to do their jobs well.

If the City wants reliable service, it has to budget for the full operating environment that makes that service possible.

Why Technology Matters

Personnel costs are only part of the equation.

The systems employees use every day have a direct impact on how efficiently government operates.

Over many years, the City purchased or inherited different software systems that do not fully work together. As a result, information often has to be entered more than once. Records may exist in multiple places. Processes that should be automated remain manual. Many City processes still rely heavily on paper.

That costs money.

Every duplicate entry requires employee time.

Every paper process slows down the work.

Every disconnected system increases the chance of error.

Every inefficient workflow increases the labor cost of running the City.

The FY2026 budget includes approximately $32,000 in explicit software and support costs. That should not be viewed only as an expense. The right software can create a real return on investment.

If better systems save staff hours each week, those hours can be redirected toward citizen service, permits, inspections, public safety administration, financial reporting, records management, infrastructure support and other real work.

Technology is not valuable because it is new.

Technology is valuable when it reduces repeated work, improves accuracy, increases transparency and allows employees to serve residents faster.

Looking Forward

The FY2026 budget reflects a different approach to municipal management.

It is a move away from simply reacting to needs and toward planning for them.

It is a move away from looking only at payroll and toward understanding the full cost of staffing.

It is a move away from disconnected systems and paper-heavy processes and toward better tools, better reporting and better accountability.

Most importantly, it recognizes that good employees are not just an expense line. They are the people who turn a budget into actual service.

A city can buy equipment, software, vehicles and buildings, but none of those things serve the public without people willing to do the work.

Success is not measured simply by spending less money.

Success is measured by delivering better services at the lowest sustainable long-term cost.

That requires understanding the true cost of employees, budgeting honestly, staffing departments appropriately, managing benefits responsibly and investing in systems that allow employees to work more efficiently.

The objective is not a larger government.

The objective is a smarter government that values its employees, respects its taxpayers and provides stronger service for the citizens of Margaret.

Leave a Reply