And Why the Structure Matters More Than the Politics

Most people only see one piece of city government at a time.

They see a police officer, a fire truck, a water bill, a road issue, a building permit, a council meeting, or a post online.

But the City of Margaret is not one simple office. It is a full municipal operation made up of two legal entities, multiple departments, elected officials, employees, state reporting requirements, public safety services, utility operations, financial controls, and several separate software systems that all have to work together.

That structure matters.

Because when the structure works, the city can plan, budget, respond, and grow responsibly.

When the structure fails, the city becomes reactive, confusing, expensive, and difficult to hold accountable.

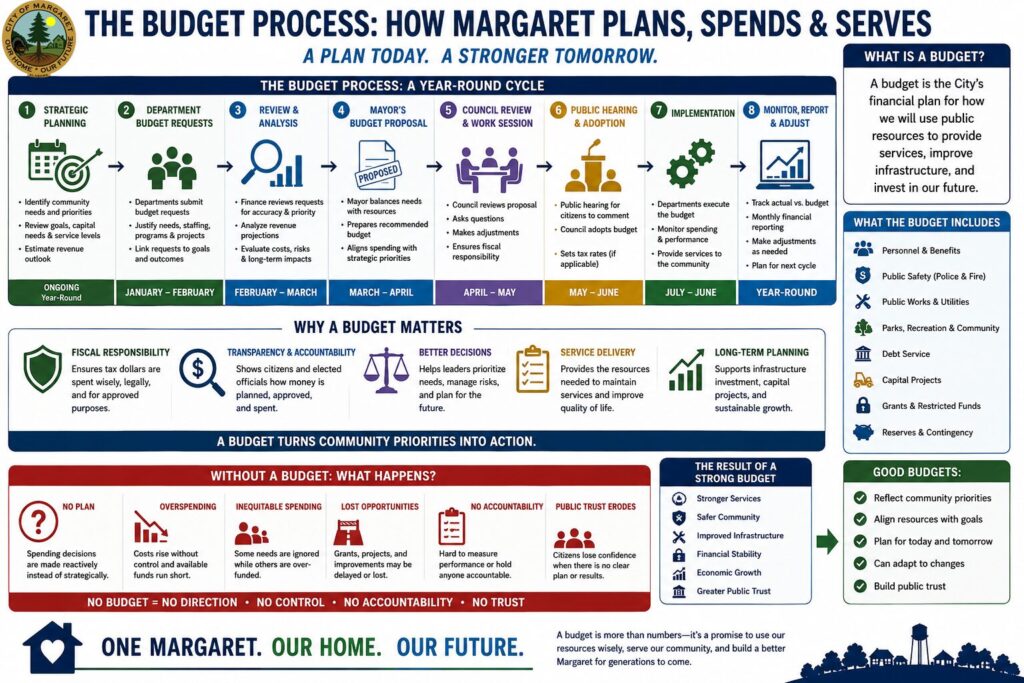

The Starting Point: No Budget, No Structure

Before discussing accountability, it is critical to understand a foundational failure:

From 2020 until November 2025, the City of Margaret operated without an adopted budget.

That means:

- No formally approved spending plan

- No alignment between revenue and expenditures

- No department-level accountability

- No benchmark to measure performance

- No true budget-versus-actual reporting

Until recently, there was no meaningful budget-versus-actual comparison because nothing had been formally adopted to compare against.

This is not just a procedural issue.

It is a structural breakdown of municipal governance.

Millions were spent across multiple administrations without council knowledge, much less approval.

A city without a budget is not truly managing public resources. It is reacting to bills, emergencies, habits, and decisions as they come.

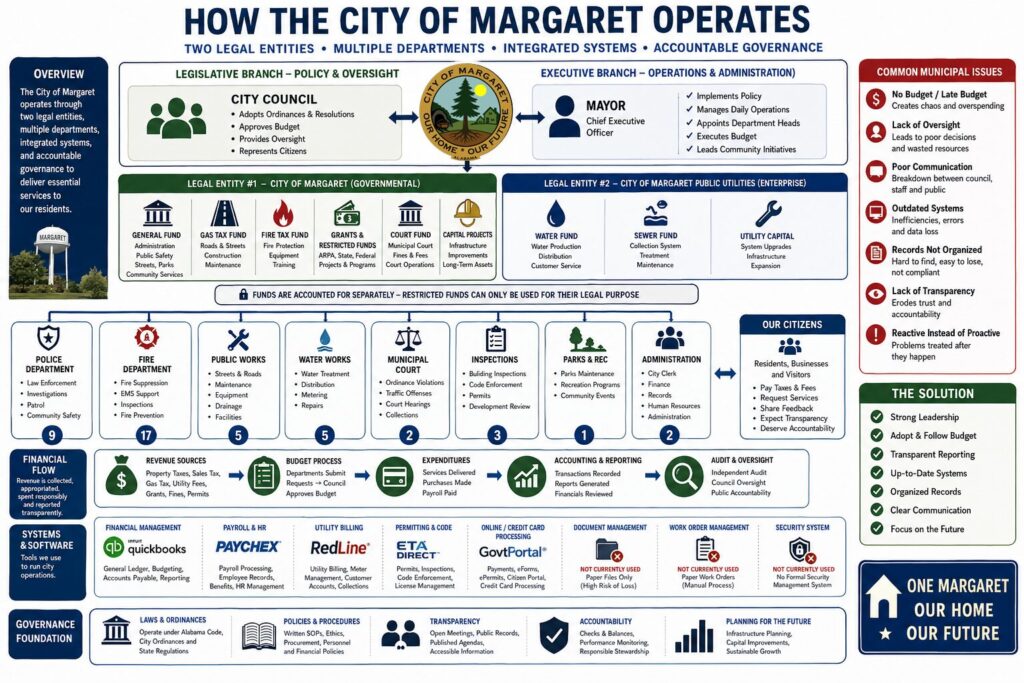

How a City Is Designed to Operate Under Alabama Law

Municipal government in Alabama follows a Mayor-Council system, which is intentionally structured around separation of powers.

Executive Branch: Mayor

The Mayor is responsible for executive and administrative operations, including:

- Overseeing day-to-day operations

- Supervising departments and employees

- Executing the budget

- Implementing policy

- Coordinating department heads

- Managing the city’s administrative direction

Legislative Branch: City Council

The City Council is responsible for legislative authority and oversight, including:

- Adopting ordinances and resolutions

- Approving the budget/appropriations

- Setting policy

- Representing citizens

- Providing oversight, not daily administration

This separation exists to prevent:

- Political micromanagement of employees

- Misuse of funds

- Confusion over authority

- Breakdown of accountability

- Council members individually directing operations outside the public meeting process

The Mayor runs daily operations.

The Council sets policy and sets appropriations.

Both roles matter, but they are not the same.

How Margaret Is Structurally Organized

The City of Margaret operates through two distinct legal and financial entities:

- The City of Margaret governmental entity

- The City of Margaret Public Utilities enterprise entity

These are connected, but they are not the same thing.

Legal Entity #1: City of Margaret Governmental Operations

This side of the city includes the traditional municipal functions funded primarily by taxes, licenses, fees, grants, and other general revenue.

This includes:

- General Fund

- Police Department

- Fire Department

- Administration

- Municipal Court

- Inspections

- Parks and Recreation

- Roads and streets

- Gas tax funds

- Fire tax funds

- Grants and restricted funds

- Capital projects

These services exist to provide public protection, public infrastructure, public administration, and quality-of-life services to residents.

Legal Entity #2: City of Margaret Public Utilities

The second legal entity is the utility system.

This includes:

- Water operations

- Sewer operations

- Utility billing

- Water infrastructure

- Sewer infrastructure

- Utility maintenance

- Utility-related capital projects

- Utility revenue and debt

This side of the city operates more like an enterprise fund.

That means it is primarily supported by user payments, not general taxes.

Residents and customers pay for water and sewer services, and those funds should be used to operate, maintain, repair, and improve the utility system.

Why the Two-Entity Structure Matters

The separation between governmental funds and utility funds is not optional.

It exists to:

- Protect restricted funds

- Prevent utility revenue from being improperly used for general government

- Prevent tax revenue from being mixed with utility operations

- Maintain compliance with accounting standards

- Allow the city to understand the true cost of each operation

- Preserve public trust

The City’s updated Chart of Accounts reinforces this structure by separating:

- Legal entities

- Funds

- Departments

- Revenue sources

- Expenditures

- Restricted purposes

That matters because every dollar should be traceable.

The city should be able to answer:

- Where did the money come from?

- What fund did it belong to?

- What department used it?

- What was it spent on?

- Was the use legal?

- Was it approved?

- Was it budgeted?

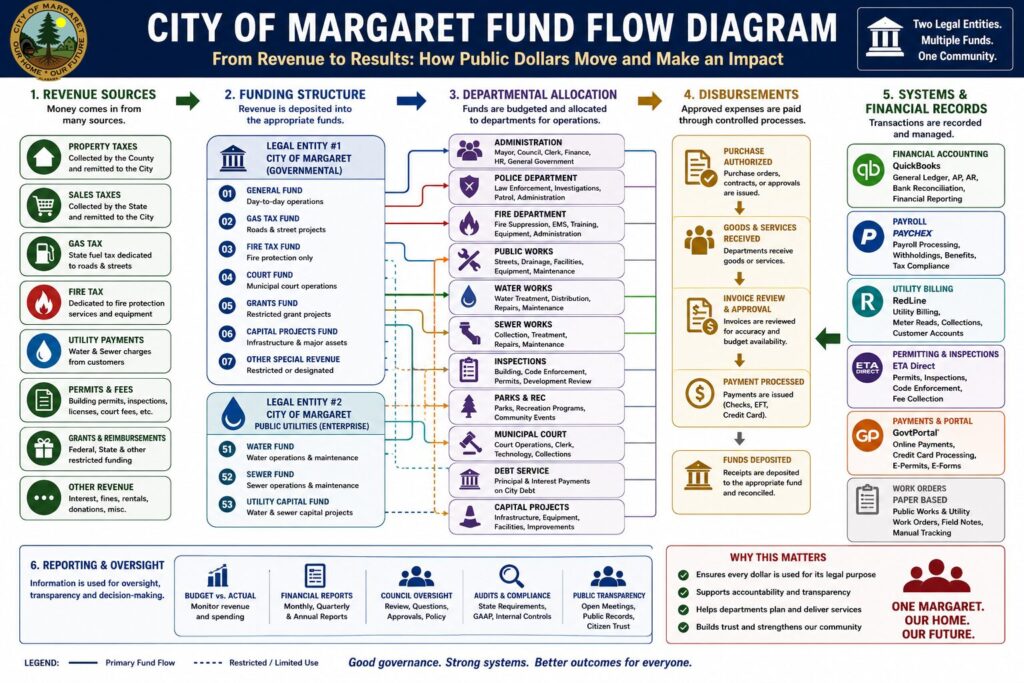

Fund Accounting: Why Municipal Money Is Not One Big Pot

Municipal finance is not like a household checking account.

A city operates through fund accounting.

That means different money has different legal purposes.

Examples include:

- General Fund: regular government operations

- Gas Tax Fund: roads and streets

- Fire Tax Fund: fire protection

- Court Fund: municipal court-related activity

- Grants: limited to approved grant purposes

- Capital Projects: long-term infrastructure and major assets

- Utility Funds: water and sewer operations

These funds are legally and operationally different.

Restricted funds cannot simply be used wherever someone wants.

That is why budgeting, accounting, reporting, and proper coding are so important.

Without fund accounting discipline, the city cannot clearly prove whether public money was used properly.

The Software Systems the City Uses

One of the biggest operational challenges is that the City of Margaret does not run on one single system.

It uses several separate systems, each handling a different part of city operations.

That is normal for many small and mid-sized municipalities, but it creates risk when there is no strong process tying them together.

1. QuickBooks: Financial Accounting

The City uses QuickBooks for financials.

This includes:

- General ledger

- Expense tracking

- Financial reporting

- Fund and department coding

- Budget reporting as the structure improves

QuickBooks is where the city’s financial activity should ultimately be reflected.

But QuickBooks is only as accurate as the information entered into it. It has largely been used like a check register and not an accounting system, but we are correcting that.

If transactions are miscoded, not reconciled, not reviewed, or not tied to an adopted budget, the reports can become incomplete or misleading.

QuickBooks is the accounting system, but it is not a substitute for governance.

2. Pchex: Payroll and Employee Records

The City uses Pchex for payroll.

This includes:

- Payroll processing

- Employee onboarding

- Wage records

- Withholdings

- Payroll deductions

- Payroll tax compliance

- Employee-related reporting

Payroll is one of the largest and most important areas of municipal spending.

Pchex can process payroll, but the city still needs internal controls around:

- Who is authorized to be paid

- What department payroll belongs to

- Whether positions are approved

- Whether raises are approved

- Whether overtime is reviewed

- Whether payroll matches the budget

Payroll software does not replace policy, approval, or oversight.

3. RL: Utility Billing

The City uses RL for utility billing.

This includes:

- Water billing

- Sewer billing

- Customer accounts

- Meter-based billing

- Utility receivables

- Utility collections tracking

This is a major system because water and sewer operations are one of the city’s largest operational responsibilities.

Utility billing directly affects:

- Monthly revenue

- Cash flow

- Infrastructure planning

- Customer service

- Delinquent accounts

- Water and sewer system sustainability

RL tracks utility billing activity, but that information must still reconcile back to the city’s accounting records.

If utility billing and accounting are not properly reconciled, the city cannot clearly understand how much money is being billed, collected, owed, or transferred.

4. ETA: Permitting and Inspections

The City uses ETA for permitting.

This includes:

- Building permits

- Inspection activity

- Contractor-related permitting

- Development review support

- Code and compliance tracking

- Permit revenue

Permitting matters because Margaret is a growing city.

Growth creates:

- New homes

- New infrastructure demands

- Road impacts

- Water and sewer impacts

- Inspection needs

- Public safety needs

- Long-term maintenance obligations

Permitting is not just paperwork.

It is one of the ways the city manages growth responsibly.

5. GPortal: Online and Credit Card Payments

The City uses GPortal for online and credit card processing.

This includes payments for things such as:

- Utility payments

- Business licenses

- Permits

- Court payments

- Fines and fees

- Other online payments

When someone pays online or pays with a card, the city is generally processing that payment through a third-party payment platform.

That creates another layer that has to be reconciled.

The city must be able to connect:

Payment made by the customer

→ payment processed through GPortal

→ payment recorded in the correct department or system

→ payment deposited into the bank

→ payment entered into QuickBooks

→ payment reported accurately

If that chain is broken, reporting becomes difficult.

6. Paper Work Orders: Public Works and Utility Field Operations

Many public works and utility work orders are still paper-based.

This includes things like:

- Water leaks

- Sewer issues

- Road complaints

- Drainage problems

- Maintenance requests

- Repairs

- Field notes

- Service requests

Paper work orders create major limitations.

They are harder to:

- Track

- Prioritize

- Search

- Report

- Assign

- Close out

- Analyze over time

- Tie to cost

- Tie to specific locations

- Tie to equipment and labor

Paper systems can work temporarily, but they do not scale well for a growing city.

If a city wants to plan infrastructure, it needs data.

Paper work orders make it harder to see patterns, such as repeated water leaks, recurring road failures, drainage hot spots, or neighborhoods with repeated service issues.

7. Manual Receipt Books and Paper Records

The city has also used manual receipt books and paper records for certain payments and processes.

This creates risk because manual systems are harder to reconcile and easier to lose, misread, duplicate, or delay.

Manual receipts require strong controls:

- Sequential receipt numbers

- Daily balancing

- Deposit matching

- Supervisor review

- Clear assignment of responsibility

- Reconciliation to accounting records

Manual processes are sometimes necessary, but they should not be the backbone of financial control.

8. Document Management: No Dedicated System

The city currently does not have a true document management system.

That means records may exist across:

- Paper files

- Local computers

- Scanned PDFs

- Shared folders

- Department files

- Council packets

- Manual records

- Vendor documents

- Historical records

This creates major problems.

Without a document management system, it becomes harder to:

- Find records

- Respond to public records requests

- Track contracts

- Locate ordinances and resolutions

- Preserve institutional knowledge

- Maintain compliance

- Support audits

- Protect the city during disputes

- Transition between administrations

Records management is not optional in municipal government.

It is part of public accountability.

The Core Problem: These Systems Do Not Fully Talk to Each Other

The city has several systems, but not one single system that contains everything.

That means information has to move across platforms.

For example:

A permit may start in ETA.

A payment may run through GPortal.

The deposit may hit the bank.

The revenue must be entered or reconciled in QuickBooks.

The inspection may be handled by staff.

The related records may be stored manually or separately.

The same is true for utilities:

A customer is billed in RL.

A payment may be processed through GPortal.

The deposit hits the bank.

The accounting entry must be reflected in QuickBooks.

A service issue may be tracked on paper.

A repair may involve labor, equipment, and materials.

That cost must eventually be tied back to the utility operation.

That is why process matters.

Software alone does not create accountability.

The city needs:

- Written procedures

- Reconciliation schedules

- Department ownership

- Budget controls

- Review processes

- Reporting standards

- Clear approval authority

- Records retention

- Audit-ready documentation

Departments and Operational Structure

A properly functioning city includes several core departments.

For Margaret, those include:

- Administration

- Police Department

- Fire Department

- Public Works

- Water Works / Utilities

- Municipal Court

- Inspections

- Parks and Recreation

Each department should have:

- Defined responsibilities

- A clear chain of command

- A budget

- Reporting expectations

- Written procedures

- Spending controls

- Performance expectations

Department heads should understand not only how to operate their departments, but also how their decisions affect the city’s budget, legal compliance, and long-term planning.

The Role of the City Council in Operations

Council authority is deliberate and limited.

The Council should:

- Approve budgets/appropriations

- Approve major expenditures

- Adopt ordinances

- Adopt resolutions

- Set policy

- Provide oversight

- Represent citizens

The Council should not:

- Run departments

- Direct employees

- Interfere with daily operations

- Make individual promises outside council authority

- Bypass the Mayor’s administrative role

- Treat operational decisions as political favors

This is what makes government action legal, transparent, and accountable.

How Margaret Has Actually Been Operating

1. Financial Breakdown

Without a budget:

- Spending occurred without a formal plan

- No department accountability existed

- No alignment between revenue and expenditures

- No true budget performance measurement existed

Even worse:

- The system had 28 bank accounts across the two legal entities

- Transactions were inconsistently categorized

- Financial reporting became fragmented

- Restricted fund tracking became harder than it should have been

Multiple bank accounts do not automatically mean something improper happened.

But too many accounts, without a strong budget and reporting structure, create confusion and risk.

2. Software and Process Breakdown

The city had multiple systems performing separate functions:

- QuickBooks for financials

- Pchex for payroll

- RL for utility billing

- ETA for permitting

- GPortal for online and card payments

- Paper work orders for field operations

- Manual records and receipt books

- No true document management system

The issue is not simply which systems were used.

The issue is whether the city had a controlled process to connect them.

Without integration and reconciliation, each system can become its own island.

That makes it harder to answer basic questions:

- How much did we collect?

- What fund did it belong to?

- Was it deposited correctly?

- Was it coded correctly?

- Was it budgeted?

- Was it approved?

- Was it spent for the right purpose?

- Is there documentation to support it?

3. Operational Breakdown

Without structure:

- Departments lacked clear leadership

- Responsibilities blurred across roles

- Work was handled reactively

- Paper systems limited tracking

- Long-term planning suffered

- Staff were forced to operate inside broken processes

Instead of:

Budget → Plan → Execute → Report

Margaret operated more like:

Spend → React → Explain later, if at all

That is not sustainable for a growing city.

4. Governance Breakdown

When structure fails:

- Oversight turns into interference

- Meetings become procedural battlegrounds

- Policy and operations blur together

- Staff become caught between politics and administration

- Residents lose confidence

And when elected officials do not consistently:

- Attend meetings

- Review financials

- Understand their role

- Participate in governance

- Respect the separation between policy and operations

The system stops functioning the way it should.

What the Data Shows

Payroll Reality

The payroll system reflects:

- Department-based payroll activity

- Standardized pay cycles

- Withholdings

- Deductions

- Employee compensation tracking

That tells us a payroll process existed.

But payroll processing alone does not equal financial control.

The city still needs:

- Approved positions

- Approved pay rates

- Department-level payroll budgets

- Overtime review

- Personnel policies

- Payroll reconciliation

- Council-approved budget authority

Revenue Reality

City revenue comes from multiple sources, including:

- Property taxes

- Sales taxes

- Business licenses

- Building permits

- Court fines and fees

- Utility payments

- Grants

- Gas tax funds

- Fire tax funds

- Other state and local revenues

Some of this revenue is flexible.

Some is restricted.

Some is recurring.

Some is unpredictable.

That is why budgeting and forecasting are essential.

A city cannot responsibly manage roads, police, fire, water, sewer, payroll, debt, and capital projects without understanding its revenue streams.

Historical Context

Audited financial statements confirm that the City is required to maintain accurate financial reporting and internal controls.

That means management is responsible for ensuring that financial statements, records, and processes are accurate and reliable.

Audits do not run the city.

They evaluate whether the city’s financial information is fairly presented.

The real work happens every day through:

- Coding

- Approvals

- Reconciliations

- Documentation

- Department oversight

- Budget monitoring

- Council review

- Internal controls

Why Structure Matters More Than Politics

This is not about personalities.

It is about whether the system:

- Protects taxpayer money

- Delivers services effectively

- Operates legally

- Supports employees

- Gives residents accurate information

- Plans for growth

- Maintains public trust

Without structure:

- Transparency becomes noise

- Accountability becomes impossible

- Financial reports become confusing

- Departments become reactive

- Council oversight becomes political

- Residents lose confidence

A growing city cannot operate on habit.

It must operate on structure.

What Is Being Fixed Right Now

This is the rebuild.

1. Financial Structure

The city is working toward:

- A real planned out budget involving each department

- A stronger Chart of Accounts

- Better fund separation

- Budget-versus-actual reporting

- Department-level accountability

- Better financial reporting to Council

2. System Alignment

The city is working to better connect:

- QuickBooks financial records

- Pchex payroll records

- RL utility billing

- ETA permitting

- GPortal payment processing

- Bank deposits

- Department reports

- Manual records

The goal is not just to have software.

The goal is to make the systems support accurate reporting and better decision-making.

3. Operational Structure

The city is working toward:

- Clear department roles

- Defined reporting lines

- Stronger department leadership

- Written procedures

- Better work order tracking

- More consistent internal communication

- Less reliance on memory and paper

4. Transparency

The city is working toward:

- Financial data being provided to Council

- Bank statements being shared with Council

- Reports being made available regularly

- Better documentation of decisions

- Clearer public communication

5. Records Management

The city is working toward:

- Cleaning up files

- Organizing historical records

- Standardizing document storage

- Making documents easier to search

- Improving access to records

- Supporting public records compliance

What Comes Next

A functioning city requires more than good intentions.

It requires systems.

1. A Real Budget

The city needs:

- Department-level accountability

- Revenue forecasting

- Capital planning

- Debt planning

- Payroll planning

- Utility planning

- Public safety planning

2. Organizational Clarity

The city needs:

- A defined org chart

- Clear reporting lines

- Written job responsibilities

- Performance expectations

- Department-level planning

3. Better Systems and Processes

The city needs:

- Digital work order tracking

- Better document management

- Better reconciliation between systems

- Written internal controls

- Standard operating procedures

- Better reporting tools

4. Council Engagement

The city needs elected officials who:

- Attend meetings

- Read financial reports

- Understand the budget

- Respect their role

- Provide oversight without interfering in daily operations

- Make decisions based on facts, not politics

The Bottom Line

Margaret is not just a small town anymore.

It is a growing city with:

- Public safety operations

- Water and sewer infrastructure

- Roads and drainage responsibilities

- Court operations

- Permitting and inspections

- Parks and recreation

- Employees and payroll

- Grants and restricted funds

- Multiple software systems

- Multiple revenue streams

- Long-term infrastructure needs

That requires structure.

That requires a budget.

That requires accountability.

That requires leadership.

And most importantly, it requires everyone to understand that the city does not operate by politics alone.

It operates through law, systems, people, processes, and public trust.

The goal is simple:

One Margaret. Our Home. Our Future.

Leave a Reply