In the first two parts of this series, we explained why rebuilding the City’s financial structure had to come first and why revenue must be separated from transfers, clearing activity, and accounting movement. Part 1 framed the inherited structural problems, and Part 2 explained why reconciled numbers matter before anyone claims “growth” or “decline.”

Now we move to the spending side of the ledger.

Because not every payment made in the current fiscal year reflects a new decision made in the current fiscal year.

Some payments reflect current operations.

Some reflect actions approved after the budget was set.

And some reflect obligations or commitments that were already in place before this administration took office.

If those categories are blended together, the public is left with a distorted picture of what is actually being spent, when it was committed, and by whom.

That is why this part matters.

What “HoldOver” Means

For purposes of this review, HoldOver refers to prior obligations or prior commitments that carried into the current fiscal year and were paid during FY2026.

In plain language:

It is yesterday’s obligation being paid with today’s check.

That does not automatically mean the expense was improper.

It does not automatically mean the payment should not have been made.

It means the obligation belongs to an earlier decision period, even if the cash leaves the account this year.

That distinction matters.

Because if prior-year obligations are paid in the current year without being identified separately, current-year spending can appear larger than it truly is.

Why This Distinction Matters

A budget is supposed to function as the City’s financial plan for the year.

But current-year disbursements are not all the same thing.

Some are:

- obligations already built into the budget,

- inherited or carried-over items,

- later approvals by council action,

- or expenditures made harder to classify because the reporting structure itself is incomplete.

If those categories are collapsed into one undifferentiated number, the public cannot tell what was inherited, what was budgeted, and what was newly chosen.

That is exactly the kind of confusion this series is intended to correct.

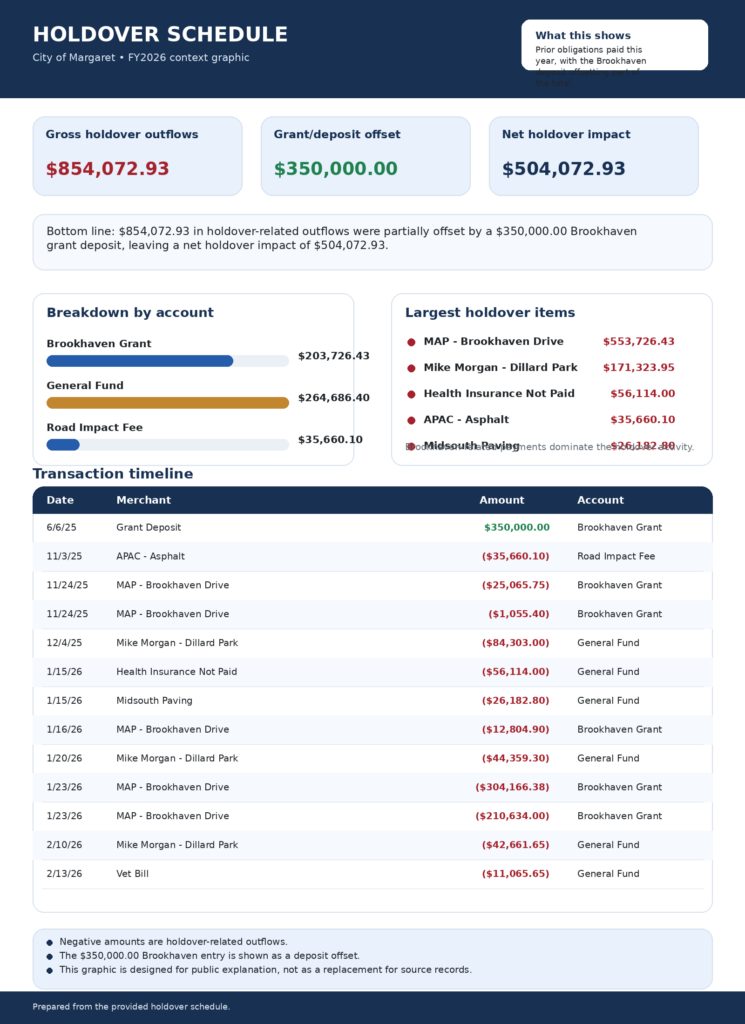

What the HoldOver Schedule Shows

The City’s holdover schedule identifies a substantial net holdover amount carried into FY2026.

That matters because it confirms something taxpayers should understand:

A payment made in FY2026 does not necessarily mean the obligation was created in FY2026.

The cash may move this year.

The obligation or commitment may have started much earlier.

And when a city is cleaning up prior commitments while also operating in the present, raw spending totals alone do not tell the full story.

Holdover schedule summary showing total/net holdover amount

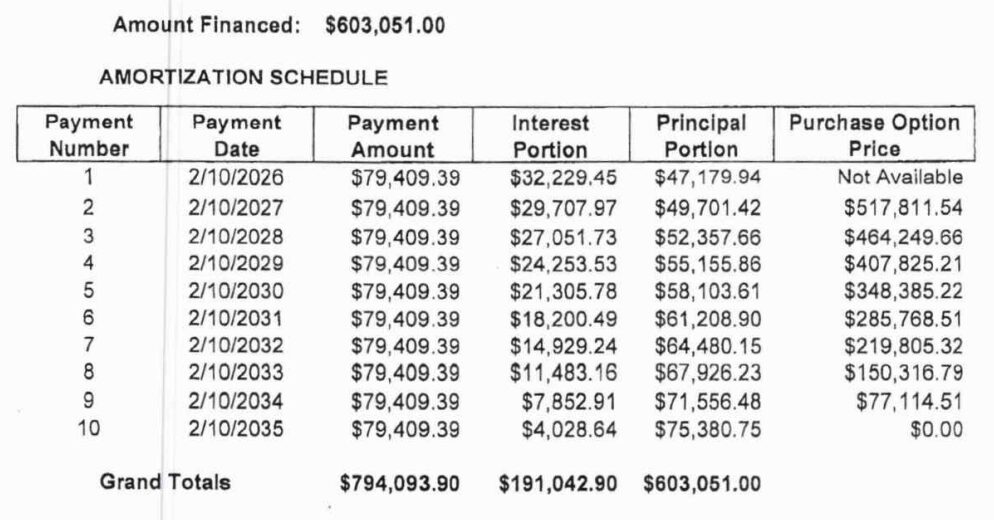

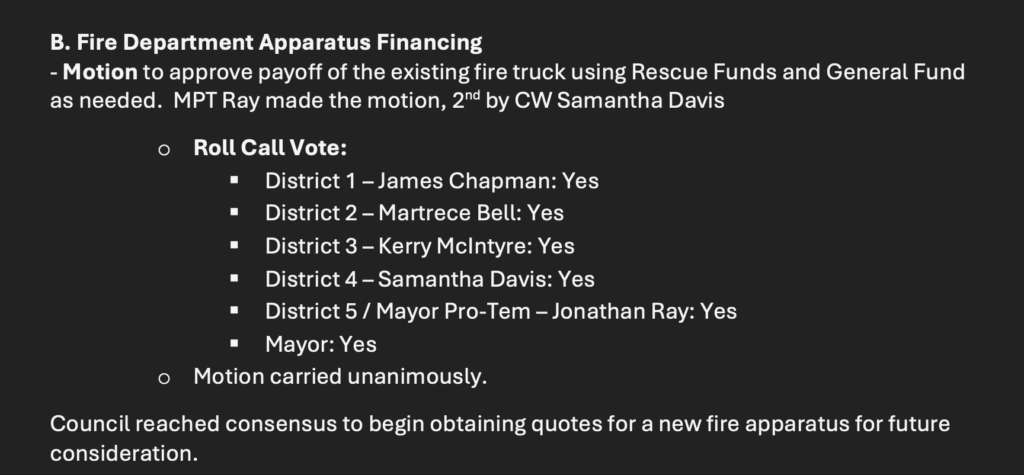

The Fire Apparatus Is a Clear Example

One of the clearest examples is the fire apparatus financing.

The financing records show a lease-purchase agreement already in place before the current FY2026 payment period. The schedule reflects approximately $603,051 financed, with total scheduled repayment of roughly $794,093.90, including about $191,042.90 in interest, and a first scheduled payment due in February 2026.

That matters because it confirms the obligation itself was not created as a fresh FY2026 spending decision.

Then, on December 15, 2025, council approved payoff of the existing fire truck using Rescue Funds and General Fund as needed.

So the FY2026 action was not the creation of the debt.

It was the decision to manage and retire an already-existing obligation more responsibly.

That is exactly the difference between an inherited obligation and new spending.

December 15, 2025 minutes showing payoff approval

Brookhaven Is Another Important Example

Brookhaven is also important because the records show it was not a project invented during FY2026.

Council action on Brookhaven predates the current fiscal year. A Brookhaven timeline compiled from the council records shows discussion going back to June 20, 2023, when the Rebuild Alabama Act grant process was requested for Brookhaven Drive. It then shows that on February 6, 2024, council approved applying for a $250,000 grant for curbs and gutters in Brookhaven Subdivision, and that motion passed with four yeses and one no. The same timeline shows that by October 15, 2024, the City had been awarded a $350,000 grant for Brookhaven Drive repairs up to Ryan Circle.

The project continued advancing before FY2026. By October 21, 2025, the City Engineer was already giving progress updates on the Brookhaven Project, stating that utility issues had been solved, storm pipe crossings had been remobilized, curbing was next, and paving would be the final phase.

That means FY2026 Brookhaven payments should be understood in context.

They are tied to a project path that had already been discussed, grant-applied, awarded, and actively progressing before those current-year disbursements occurred.

Again, the cash may move in FY2026.

But the project commitment did not begin in FY2026.

And the initial $250,000 approval toward Brookhaven matters because it shows this was not a sudden or improvised current-year initiative. It was part of an earlier council-approved funding path that later evolved into a larger project structure.

February 6, 2024 minutes showing approval to apply for $250,000 for Brookhaven

Brookhaven timeline/grant summary showing June 2023, February 2024, and October 2024 milestones

October 21, 2025 minutes showing Brookhaven project progress update

The Budget Timeline Still Matters

The later minutes also show why spending clarity has been difficult.

On November 17, 2025, the council approved the proposed budget effective immediately, with the understanding that it could later be amended. The same meeting record also notes that Brookhaven “should be completed by next week,” which reinforces that Brookhaven was already an active project by that point.

On January 5, 2026, the Annual Budget Ordinance and General Ledger Account Restructuring Resolution were formally presented again among the proposed ordinances.

Then, on January 26, 2026, the council voted to table the Annual Budget Ordinance until July and also table the General Ledger Account Restructuring until July.

That sequence matters.

It shows the City was operating in a period where a working budget existed, but structural financial reforms and formal ordinance cleanup were still catching up.

That overlap makes it harder for taxpayers to distinguish between:

- originally budgeted spending,

- inherited obligations,

- later council approvals,

- and spending made harder to classify because the reporting structure itself was incomplete.

November 17, 2025 minutes showing proposed budget approved effective immediately.

January 5, 2026 minutes showing first presentation of Annual Budget Ordinance and GL restructuring

January 26, 2026 minutes showing Annual Budget Ordinance and GL restructuring tabled until July

Budgeted vs. Later-Approved Spending

The minutes also show that current-year spending included later council action on multiple items after the initial November budget approval.

For example:

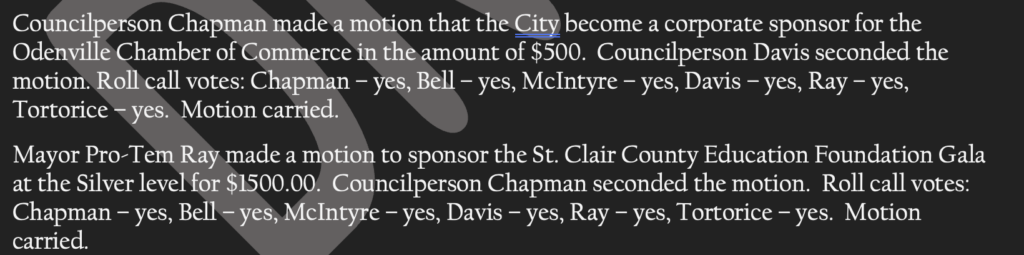

- on December 30, 2025, council addressed emergency road repairs, Public Works staffing, infrastructure issues, and Public Works equipment;

- on February 2, 2026, council approved chamber sponsorship, a gala sponsorship, Smartboards for Margaret Elementary, conference attendance, National League of Cities participation, and speed tables.

- on February 16, 2026, council adopted the Public Works truck and trailer resolution.

Those actions are not all the same category.

Some are debt management.

Some are operational response.

Some are new approvals.

Some may be tied to budgeted line items, while others clearly required later action.

If they are all blended into one undifferentiated “current spending” narrative, the public loses the ability to tell what was inherited, what was planned, and what was newly chosen.

February 2, 2026 minutes showing multiple later-approved expenditure items

Why Structural Deficiencies Affect Spending Clarity

This brings the series full circle.

Part 1 explained that the City inherited reporting systems that did not align cleanly with the budget and a financial structure that did not consistently support transparent reporting. Part 2 explained how classification issues distorted revenue totals and required reconciliation before current-year numbers could be trusted.

The same problem affects spending.

If inherited obligations are not tagged separately, if pre-existing project commitments are mixed with current operating disbursements, and if later council approvals are not clearly mapped against the adopted budget, then expense reports stop being decision tools.

They become interpretation exercises.

And taxpayers should not have to guess.

Why This Matters

Taxpayers deserve to know the difference between:

- money spent because a prior obligation had to be paid,

- money spent because it was already budgeted,

- and money spent because a new decision was made.

Those are not political distinctions.

They are accounting distinctions.

And they are essential to honest public reporting.

If inherited obligations are blended into current-year discretionary spending, the public gets a false picture of present decision-making.

If later approvals are blended into the original budget narrative, the public cannot judge fiscal discipline accurately.

And if structural deficiencies prevent reliable classification, then confusion fills the space where transparency should be.

We are correcting that.

What Comes Next

In the next installment, we will go one step further and examine actions approved after budget adoption, operational expansions, department startup costs, and the financial effect of decisions made outside the original plan.

Not through opinion.

Through records.

Because responsible financial governance requires more than numbers on a page.

It requires that those numbers mean what they appear to mean.

And we will continue to show our work.

Leave a Reply